Part 4: Risk identification and mitigation

4.1

In this Part, we:

- state our expectations;

- describe the main risks;

- assess councils’ risk management strategies; and

- consider the application of certain Acts to rates postponement.

What we expected

4.2

We expected that, in developing a rates postponement policy, councils would

have:

- identified both short-term and long-term risks associated with the policy; and

- put in place strategies to manage these risks.

Main risks of rates postponement schemes

4.3

During our audit we identified several significant risks. This section describes how

these risks apply to rates postponement generally. Paragraphs 4.16–4.48 describe

the councils’ risk management strategies.

Risk of reduced cashflow

4.4

When councils allow ratepayers to postpone rates, they are reducing their

cashflow by the amount of rates postponed every year. Currently, none of the

councils we audited has more than $130,000 in outstanding postponed rates. Although this represents reduced cashflow, the amounts are small enough to

be comfortably covered by existing cashflows and borrowing arrangements. However, if the number of ratepayers postponing their rates increases

substantially, councils will need to have a way of forecasting and funding the

reduced cashflow.

Risk that properties that rates are postponed against are not insured

4.5

Postponed rates are secured against the equity in the ratepayer’s property. If an

uninsured property suffered a fire or other catastrophic event, the value of the

property would be reduced and the council might not be able to recover the full

value of the postponed rates.

4.6

Related to the insurance risk is a maintenance risk. The value of improvements can

be eroded by a lack of maintenance. This may be a particular risk in the case of

ratepayers suffering financial hardship.

4.7

It is unlikely that the current value of any postponed rates on an individual

property owed to the councils we audited exceeds the unimproved value of

the property. In these cases, the value of the land would be enough to pay the

postponed rates. However, over time, the amounts owed by individual ratepayers

are likely to increase and may exceed the unimproved value. Councils therefore

need to have systems in place to check ratepayers’ house insurance.

4.8

As well as risks of a financial nature, there is a risk to councils’ reputations. In

the event that an uninsured house on a property that rates had been postponed

against suffered a catastrophic event, the council would have a valid legal claim

on the value of the land and would thus be entitled to recover at least a portion

of the postponed rates. However, recovering the postponed rates might leave

very little or no equity for the ratepayer. If this situation arose, councils could

be exposed to adverse publicity and accusations that they had acted against

the interests of the ratepayer by allowing them to postpone their rates but not

requiring them to insure their house.

Risk that the value of postponed rates may exceed the final sale value of the property that they are postponed against

4.9

Councils postpone rates in the expectation that the rates will eventually be

collected when the property that they are postponed against is sold. The council

will lose money if the value of the postponed rates exceeds the value of the

property when it is sold. Councils therefore need, at the time of application, to

assess the likely total of postponed rates, and then monitor individual accounts

so they can consider ceasing to postpone rates if the value of postponed rates

approaches the value of the available equity.

Risk of challenges to the validity of individual rates postponements based on claims of coercion by the council or failure to fully inform the ratepayer

4.10

For many older people, their property is their major asset. Ratepayers who

postpone their rates are effectively converting a portion of the equity in their

property into debt. This means that the ratepayer does not have that equity

available to buy another property or to pay for other needs such as healthcare. Rates postponement may also affect ratepayers’ families, who may receive less

inheritance because a portion of the estate will be used to pay postponed rates.

4.11

Issues such as compounding interest and the fees that are added to the

postponed rates could potentially cause misunderstanding or confusion for some

ratepayers.

4.12

For these reasons, there is a risk that ratepayers or their families or estates might

challenge the legitimacy of individual rates postponements by suggesting that

the ratepayers were coerced into postponing their rates, or that they did not fully

understand the implications of rates postponement. This issue is particularly

sensitive for councils because, as public entities, they are expected to uphold high

standards for dealing with the public.

4.13

Should a council face a claim by the ratepayer or their family of undue influence

or unconscionable behaviour, a strong factor in the council’s favour would be that

the ratepayer had received independent advice.

4.14

Councils also need to be aware that some properties may have multiple owners. All owners should be aware of, and agree to, rates postponement before the

postponement proceeds.

4.15

We consider councils’ management of this risk as part of our discussion regarding

informing ratepayers, in Part 5. See paragraphs 5.30-5.45 for a discussion of how

consortium councils manage this risk, and paragraphs 5.60-5.66 for a discussion

of how this risk is managed by the two councils we audited that offer rates

postponement on hardship grounds only.

Risk management strategies of councils with optional rates postponement policies

Risk of reduced cashflow

4.16

We discussed with the consortium councils how they intended to forecast and

fund the reduced cashflow that results from rates postponement.

4.17

None of the four consortium councils we audited, nor the rates postponement

consortium as a whole, had devised a robust method to forecast the effect of

postponed rates on their future cashflow, although Gisborne District Council did

include an estimate of outstanding postponed rates for the next 10 years in its

2006-16 LTCCP.

4.18

The reduction in council cashflow may stabilise over the long term, as roughly

equal numbers of ratepayers enter the scheme (begin postponing their rates) and

exit the scheme (pay the total amount of rates that have been postponed against

their property). However, this could not be expected to happen for a number of

years, given the current growth of the scheme. Furthermore, even if the reduction

in cashflow stabilises, councils will still have an amount of postponed rates

outstanding at any one time and will need to fund that deficit.

4.19

Because the value of postponed rates is so low at present, councils are managing

the reduced cashflow within their normal cashflow arrangements.

4.20

There are various options councils may consider in the future for funding the

reduction in cashflow created by rates postponement. However, current rates of

participation in optional rates postponement mean that councils are unlikely to

need to make a decision on this issue for some years.

On-balance sheet borrowing

4.21

Some councils told us that, if the number of ratepayers postponing their rates

grew substantially, the amount of borrowing needed to fund the deficit could be

inconsistent with borrowing limits in their current liability management policies.

4.22

However, the consortium told us that councils may consider making amendments

to their liability management policies to enable additional on-balance sheet

borrowing to fund the deficit caused by rates postponement. The liability

management policies could be amended so that this borrowing is separate from

borrowing for normal capital purposes.

Securitisation

4.23

During the audit, some councils indicated that they may not wish to fund the

deficit through on-balance sheet borrowing. If this is the case, one option councils

might investigate is securitising the debt.

4.24

The consortium has discussed securitisation as a way of funding the cashflow

deficit. Securitisation involves a council selling securities to the third party, using

the outstanding postponed rates as collateral. Ratepayers still owe their rates to

the council, but the council then owes the money it collects in postponed rates to

the third party. This arrangement provides councils with a predetermined annual

cashflow to cover the cashflow lost through postponed rates. By selling the debt

to a third party, it may be possible for councils to stay within any borrowing limits

set out in their liability management policies.

4.25

We were told by the consortium management company that securitisation may

become a realistic option if the total amount of postponed rates reaches $5

million across the consortium as a whole. Once that initial parcel of debt has

been securitised, councils may be able to issue further securities in tranches of

approximately $2.5 million.

4.26

Securitisation may involve changes to the cost of borrowing. Under their policy of

user pays, councils offering optional rates postponement would pass on the cost

changes to the ratepayers in the scheme.

| Recommendation 3 |

|---|

| We recommend that councils that experience a substantial growth in the number of applications for rates postponement devise a method of forecasting the effect of rates postponement on their future cashflow and make provision for funding this deficit. |

Risk that properties that rates are postponed against are not insured

4.27

It is a condition of optional rates postponement that ratepayers insure their

houses. This helps to protect the council’s security. However, only one of the four

consortium councils we audited planned to regularly check that ratepayers had

current insurance.

| Recommendation 4 |

|---|

| We recommend that all councils that offer optional residential rates postponement require ratepayers to provide annual proof that their house is insured as a condition of continued postponement. |

4.28

The rates postponement consortium is currently finalising a basic insurance policy,

which will be offered to ratepayers who wish to postpone their rates but who do

not have insurance on their house. The councils intend to add the premiums for

this policy to the outstanding rates.

4.29

Councils need to ensure that the way they charge ratepayers for the premiums

for this insurance policy complies with the provisions in the Local Government

(Rating) Act 2002 regarding charging fees for postponing rates.

4.30

One council suggested to us that they might recover the cost of this insurance

through a targeted rate. In our view, this would stretch the purpose of targeted

rates and is unlikely to be practical.

4.31

However, we consider that, if the council pays the insurance premiums, the cost

should be recovered from the ratepayer concerned as part of the administration

costs of rates postponement.

| Recommendation 5 |

|---|

| We recommend that councils organise insurance arrangements so that the premiums for a council-organised insurance product can be legally added to the postponed rates. |

Risk that the value of postponed rates may exceed the final sale value of the property that they are postponed against

The actuarial model

4.32

The rates postponement consortium has developed an actuarial model that, used

with standard New Zealand life expectancy tables, enables councils to estimate

how much equity will be left in a given property at the end of a ratepayer’s

estimated life expectancy.

4.33

The councils use the results from the model for two purposes:

- to assess whether an applicant is likely to have enough equity to meet the council’s eligibility criteria; and

- to inform the ratepayer about the likely effect of rates postponement on their equity.

4.34

The details of all applications are run through this model using the council’s

default assumptions regarding the interest rate, the rate of growth in property

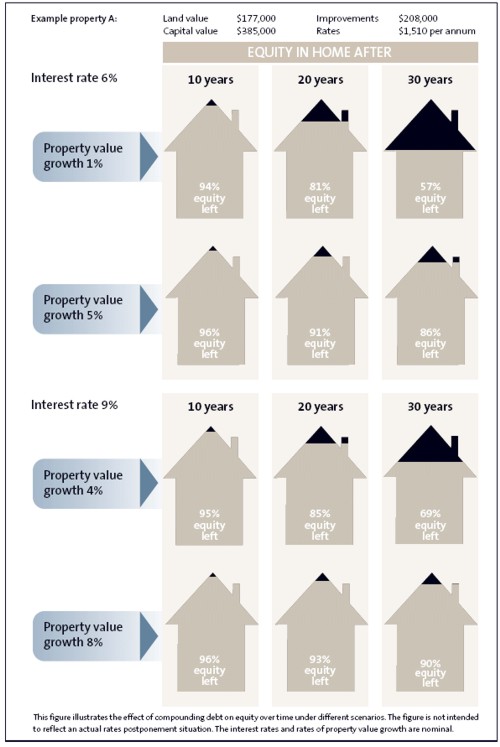

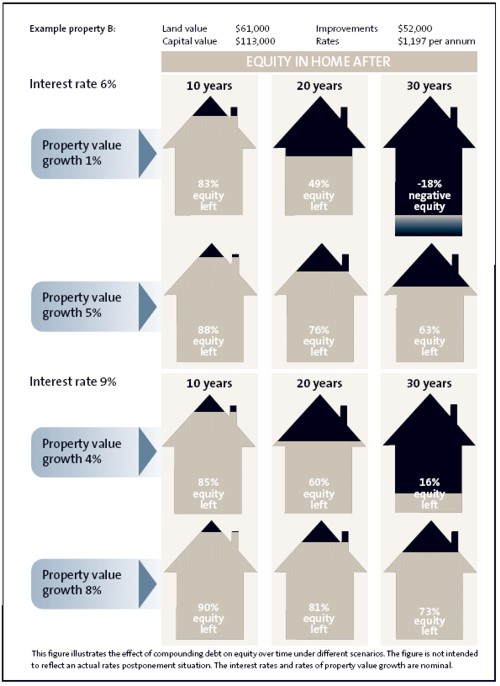

values, and the rate at which rates will increase. As shown in figures 1 and 2 (following paragraph 2.34), the results are sensitive to different assumptions

about interest rates and rates of property value increase.

{kind=link}

{kind=link}

4.35

Rates postponement is granted only if the model suggests that total postponed

rates (including interest and fees) will not accumulate to more than 80% of

the equity in the property. If the total is likely to exceed 80%, partial rates

postponement may be offered. In this way, councils manage the risk of the value

of postponed rates exceeding the value of the property they are postponed

against.

4.36

For the purposes of determining eligibility, it is reasonable for councils to use

assumptions that reflect the most likely scenario.

4.37

However, there is a risk that applicants may have an unjustified sense of comfort

about the certainty of the actuarial results generated by the council.

| Recommendation 6 |

|---|

| We recommend that councils using an actuarial model ensure that applicants understand that the results from the model are a forecast only, and depend on the accuracy of the assumptions used to generate them. |

| Recommendation 7 |

|---|

| We recommend that councils using an actuarial model ensure that applicants have seen and understood both “high effect” and “low effect” results from the model. |

| Recommendation 8 |

|---|

| We recommend that councils using an actuarial model regularly review the default assumptions used in the model to ensure that they reflect the best available information. |

4.38

We discuss the actuarial model, choosing appropriate assumptions, and

generating “high effect” and “low effect” results further in Appendix 4.

The reserve fund fee

4.39

Despite the use of the actuarial model, in individual cases, selling the property

may raise less than expected or the ratepayer may live much longer than

expected. In some cases, this could mean that there is a shortfall between the

rates that the council is owed and the proceeds of selling the property. The council

would have to bear any such shortfall, because optional rates postponement

comes with a “no negative equity” guarantee for the ratepayer. No matter how

much the debt is, the ratepayer or their estate does not have to pay the council

more than the amount raised from selling the property.

4.40

To offset the risk of these individual cases, councils charge all ratepayers who

postpone their rates an annual 0.25% reserve fund fee, which is added to the

postponed rates. This reserve fund is insurance for the council. Each consortium

council manages its own reserve fund.

4.41

The current rate of the reserve fund fee is provisional, based on initial predictions

of the appropriate rate to adequately cover the risk of bad debts. The consortium

intends to have the fee reviewed by an actuary in two to three years, when the

scheme has been running for longer and there is more data to base projections on.

4.42

As reserve funds build up, the consortium will need to consider creating guidelines

for how these funds should be managed.

Risk management strategies of councils with hardshiprates postponement policies

Risk of reduced cashflow

4.43

The two councils we audited that offer rates postponement on hardship grounds

only are able to cover the current low value of postponed rates from their existing

cashflows and borrowing arrangements. This situation appears unlikely to change

in the short term.

4.44

If these councils were to experience a significant increase in the number of

ratepayers postponing their rates on the grounds of hardship, they would need to:

- forecast the likely total of outstanding postponed rates to assess the possible effect on cashflow; and

- consider the funding implications, including what is permitted by their liability management policies.

Risk that properties that rates are postponed against are not insured

4.45

Not all policies of rates postponement on the grounds of hardship require that

ratepayers insure their houses as a condition of postponement. Of the two

councils we audited that offer rates postponement on hardship grounds only,

Wellington City Council requires ratepayers postponing their rates to insure their

houses, but Christchurch City Council does not.

| Recommendation 9 |

|---|

| We recommend that all councils that offer residential rates postponement outside the rates postponement consortium require ratepayers to provide annual proof that their house is insured as a condition of continued postponement. |

Risk that the value of postponed rates may exceed the final sale value of the property that they are postponed against

4.46

The two councils that we audited offering rates postponement on the grounds of

hardship only did not undertake a formal assessment of the likely total debt the

ratepayer would incur through rates postponement. They were therefore not able

to accurately assess the risk of the value of postponed rates exceeding the value of

the property that they are postponed against.

4.47

Hardship policies have explicit social objectives, and the numbers of ratepayers

postponing their rates on the grounds of hardship are likely to remain low. It is

therefore reasonable for councils to accept the risk that the value of postponed

rates may exceed the value of the property that they are postponed against. We

do not consider that councils offering postponement on the grounds of hardship

need to instigate a reserve fund fee on postponed rates.

4.48

However, it is important for councils to be aware of the likely total amount of

postponed rates, including interest and fees, over the time individual ratepayers

continue to postpone rates. This will allow councils to:

- inform ratepayers more accurately about the implications of postponing rates; and

- assess more accurately whether the ratepayer is likely to have enough equity in their property to cover the postponed rates.

| Recommendation 10 |

|---|

| We recommend that councils offering rates postponement outside the rates postponement consortium assess the likely total amount of postponed rates, including interest and fees, for individual ratepayers at the time of application. |

Rates postponement and certain Acts

4.49

In this section, we consider whether the Credit Contracts and Consumer Finance

Act 2003, the Bill of Rights Act 1990, and the Human Rights Act 1993 are relevant

to both types of residential rates postponement policies.

Credit Contracts and Consumer Finance Act 2003

4.50

The Credit Contracts and Consumer Finance Act 2003 imposes various disclosure

and other requirements on a “consumer credit contract”.

4.51

In our view, the Credit Contracts and Consumer Finance Act does not apply to

rates postponement, on the basis that section 11(d) of the Act – in the definition

of a “consumer credit contract” – does not apply to councils. Section 11(d) refers

to the creditor carrying on a business of providing credit, or making a practice of

providing credit in the course of carrying on a business.

4.52

By offering a rates postponement scheme, a council may be in the practice of

providing credit, but not in the course of a business carried on by the council. The scheme is being offered in connection with councils’ statutory powers to set,

assess, and collect rates. While a council has full capacity to undertake any activity

or business (subject to the Local Government Act and other applicable law), we do

not think that collecting rates constitutes a “business” as such.

New Zealand Bill of Rights Act 1990 and Human Rights Act 1993

4.53

Some councils offering rates postponement offer it only to ratepayers over

a certain age – generally 65 but, in one case, 60. Other councils offer rates

postponement to younger ratepayers, but only for a set term of up to 15 years.

4.54

Age (over the age of 16 years) is a prohibited ground of discrimination under the

Human Rights Act 1993. The right to freedom from discrimination, including on

the grounds of age, is affirmed in the New Zealand Bill of Rights Act 1990.

4.55

Section 5 of the Bill of Rights Act places justifiable and reasonable limitations on

the rights and freedoms contained in that Act, such as the right to freedom from

discrimination. This means that different treatment on the grounds of age will not

be improper if it can be objectively and reasonably justified.

4.56

Councils target rates postponement to older ratepayers because older ratepayers:

- are likely to be retired and on modest fixed incomes;

- are likely to have significant equity in their properties; and

- have a shorter life expectancy, resulting in the debt being postponed for a relatively short period of time.

4.57

Offering rates postponement to ratepayers over the age of 65 years is consistent

with the eligible age for New Zealand superannuation, and 65 may therefore be

an appropriate age to differentiate between different groups of people for this

purpose. However, selecting an age other than 65 (such as 60) is more arbitrary,

and may be difficult for councils to justify if challenged.

4.58

Another potential issue is that, if a person in a comparable situation to older

ratepayers – for example, a 55-year-old unemployed person with significant equity

in their property – was denied rates postponement because of their age, they

might be able to argue that discrimination had occurred.

4.59

Those councils that have a suggested age limit, but note that exceptions are

possible, would be able to make an exception to cover such a case. Councils that

offer limited-term postponement to ratepayers under their age limit would also

be able to accommodate this situation.