Appendix 4: The actuarial model used by the rates postponement consortium

The purpose of the actuarial model

Consortium councils use the actuarial model to assess whether there is likely to be sufficient security available in the applicant’s property to cover the estimated total of outstanding rates at the end of the period of postponement. If the model shows that ratepayers are unlikely to have enough equity to cover the total amount of postponed rates, they will either be offered partial postponement to the level sustainable by their equity or have their application denied.

This assessment allows the councils to minimise the risk of allowing ratepayers to postpone a greater amount of rates than they are able to pay using the equity in their property.

Results from the model also allow councils to inform ratepayers about the likely effect of rates postponement on their equity.

How the model works

The actuarial model was developed for the consortium by an actuary. It has since been updated to make it easier to use and to incorporate the new central government rates rebate scheme.

The actuarial model incorporates the following variables:

- annual rates;

- interest rate;

- one-off fees;

- annual fees;

- reserve fund levy;

- insurance premiums;

- annual rates rebate for qualifying ratepayers; and

- rate of increase in property values.

An allowance for inflation is also included.

The model allows different assumptions to be entered for up to five years and beyond five years. Each council changes these assumptions to accord with their district’s experience – for example, some districts may expect higher rates of increase in property values than other areas.

The model uses Statistics New Zealand life tables to estimate the life expectancy of the applicant. Where two applicants apply jointly, the longest life expectancy is taken as the term of postponement.

How the model is used

Each council has a default set of assumptions that they use when running the model.

Information regarding an application, such as the applicant’s age and the current value of their property, is fed into the model. The result is a spreadsheet showing the cumulative percentage of the ratepayer’s equity that will be consumed by postponed rates in a given year if the assumptions used in the model are correct. The final year of estimated life expectancy is highlighted, indicating the total amount of equity likely to be consumed by postponed rates if the ratepayer remains alive until that time.

The councils use the results from the model for two purposes – to assess whether an applicant is likely to have enough equity to meet the council’s eligibility criteria, and to inform the ratepayer about the likely effect of rates postponement on their equity.

If the results from the model show that the amount of equity likely to be consumed by rates postponement is under 80%, councils will grant full postponement. If it is over 80%, they may offer partial postponement or decline the application.

A copy of the results spreadsheet is sent to the ratepayer when they are advised of the outcome of their application.

If the application has been approved, another copy is sent to Relationship Services, to allow the decision facilitator to prepare for the decision facilitation session.

Decision facilitators have access to a live version of the model for use during decision facilitation sessions. This means they can show applicants the effect of different assumptions – for example, how much more equity would be used if applicants lived longer than expected, or if interest rates were higher than the default setting used by the council.

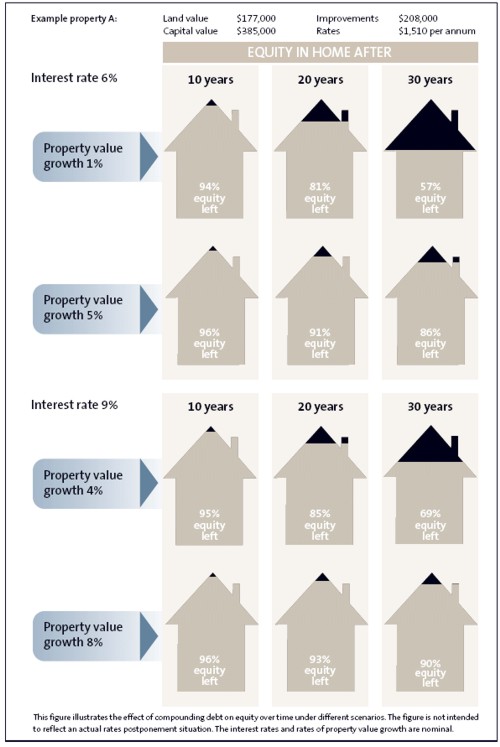

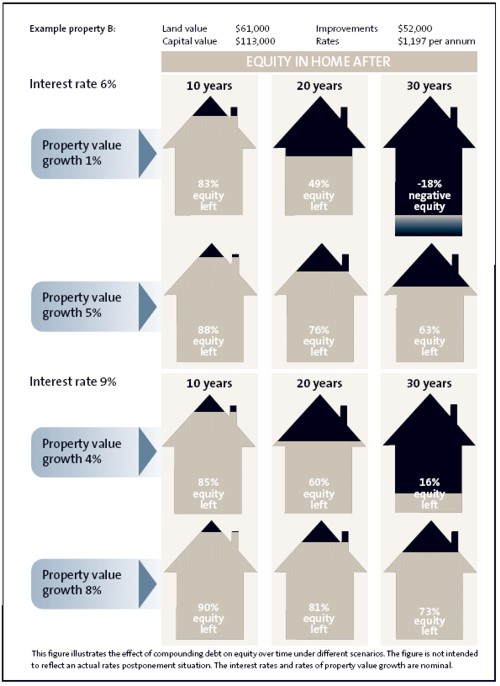

The effect on ratepayers’ equity of the gap between interest rates and the rate of increase in property values

Under normal circumstances, interest rates will be higher than the rate of increase in property values over the long term. The size of this gap between interest rates and property value increases is the most important factor in determining how much equity will be used up by rates postponement over a given length of time.

The greater the difference between the interest rate and the rate of property value increase, the greater the effect on the ratepayer’s equity. This is because the interest will be building up more quickly than the value of the property is increasing.1

Conversely, the closer the rate of property value increase is to the interest rate, the less the effect rates postponement will have on the ratepayer’s equity. This is because the effect of compounding interest is being mitigated by the increase in the value of the property.

The effect of this gap on the results predicted by the model becomes more accentuated over longer periods of time. Figures 1 and 2 in Part 2 show this effect.

{kind=link}

{kind=link}

The gap between assumed interest rates and rates of property value increase over the longer term varied widely among councils. Western Bay of Plenty District Council assumed that the rate of property value increase in its district would be 5% lower than interest rates over the long term. Rodney District Council assumed a higher long-term rate of property value increase, creating a gap of only 1.5% between rates of property value increase and interest rates.

Our review of the model

Accuracy of the model

The actuary we consulted prepared an alternative model to test the results generated by the consortium’s model. There were no material differences between his results and the results from the consortium’s actuarial model.

Using the model to determine eligibility for rates postponement

The actuarial model results show what will happen in a given scenario. However, the results are a forecast – not a set of guaranteed actual outcomes.

For the purposes of determining eligibility, it is reasonable for councils to use assumptions that reflect the most likely scenario.

Currently, assumptions for the actuarial model are generated by individual councils. Property value assumptions are based on recent historical experience and a council’s view of likely future property value increases in its district. While this may be a reasonable basis for short-term forecasts, these factors are less likely to be appropriate as the basis for longer-term forecasts of up to 30 years.

Likewise, current and recent interest rates are not necessarily a good guide to likely interest rates over the long term, particularly as there is no market rate for interest beyond 10 years.

An alternative way of generating long-term rates of property value increase and interest rates would be to use inflation (the Consumer Price Index) as a base for estimating future property price increases and interest rates. Using this method, the important assumption is the real rate of property price increase, which is added to the long-term inflation rate to produce the nominal rate of property price increase. Similarly, the assumed nominal interest rate is set by adding assumed real interest rates to the rate of inflation. This approach creates internal consistency between the assumptions, and ensures that the gap between rates of property value increase and interest rates will be within a reasonable range.

It is important that councils continue to review the default assumptions used to assess ratepayers’ applications. In our view, councils should regularly discuss these assumptions with other members of the consortium, and seek professional advice if they consider it is required.

We note that the model also requires councils to enter a variable for the rate at which rates are going to increase. Councils should ensure that the level of rates inflation assumed in the model reflects the increases they have planned in their LTCCPs. We were told that consortium councils are currently doing this.

There may be benefit in councils periodically running existing ratepayer accounts through the model, particularly if there are significant changes in the assumptions. This would allow councils to see how the new assumptions affect existing rates postponement accounts as well as new applications.

Using the results from the model to inform ratepayers about the possible effect on their equity

The consortium councils send applicants one set of results generated by the actuarial model. These results are a forecast based on the council’s view of the most likely scenario, but they are not a guaranteed result. The accuracy of the results generated by the actuarial model depends on the accuracy of the assumptions used.

In our view, councils need to ensure that applicants understand that the results from the model are a forecast only, and depend on the accuracy of the assumptions used to generate them.

Applicants who choose to continue with rates postponement attend a decision facilitation session at which the decision facilitator has access to a live version of the actuarial model. However, facilitators are not explicitly required to explain that the accuracy of the actuarial model’s results provided by the council depends on the accuracy of the council’s assumptions. Nor are they required to show applicants the effect of using different assumptions in the model.

As noted above, the gap between the assumed interest rate and the assumed rate of property value increase is the most important factor affecting the results from the model over the long term. Higher interest rates in relation to the rate of property value increase will mean that rates postponement will use a greater proportion of the ratepayer’s equity. Less equity will be used if the interest rate is lower or the rate of property value increase is greater.

For example, a council’s default assumptions for assessing eligibility might be an interest rate of 8% and a property value increase of 4% (giving a 4% gap between the interest rate and the rate of property value increase). In this case, a “high effect” result could be generated using a property value increase of 2% (giving a 6% gap between the interest rate and the rate of property value increase). A “low effect” result could be generated using a property value increase of 6% (giving a 2% gap between the interest rate and the rate of property value increase).

Councils need to ensure that applicants have seen and understood both “high effect” and “low effect” results from the model.

1: It should be noted that the value of outstanding postponed rates on which the interest is being incurred will be much less than the value of the property. Therefore, a low percentage increase in the value of the property may be greater, in absolute terms, than a higher percentage increase in the value of the outstanding rates.

page top